The impending inflation and rise of interest rates are upon us, with the United States Federal Reserve looking to raise interest rates as early as March 2022.

Singapore pegs its interest rates close to that of the US, so we’re likely to see our interest rates edge higher as well. UOB economists predict that the key benchmark rate of SORA might shoot from 0.25% in Q1 2022 to 1.01% by the end of the year.

What does this mean?

This means that if you currently have a mortgage, your mortgage payments will be higher. Mortgage loans make up more than 75% of a household’s monthly recurring expense. MAS advises households to be mindful of their ability to service mortgage obligations. It is also recommended that highly leveraged households should build up financial buffers.

Singapore’s current benchmarks

Right now, the most common interest rate benchmarks are the Swap Official Rate (SOR) and Singapore Interbank Offered Rate (SIBOR). They’ve served as the cornerstones for interest rates for at least two decades, since the late 1990s.

We’ve covered the differences between SOR and SIBOR in-depth here.

1. Transitioning to SORA

SOR and SIBOR are currently phasing out to make way for SORA. As of March 2021, the option for SORA has been rolled out by most major banks, with more than S$1 billion of such loans extended so far.

The MAS has formed the Steering Committee for SOR & SIBOR Transition to SORA (SC-STS). It consists of a main Steering Committee comprising senior representatives from key banks in Singapore, relevant industry associations, and the MAS.

The SC-STS’ role is to ease an industry-wide transition from SOR to SORA. Industry participants include commercial and retail customers (such as homeowners with current bank loans).

Here are some deadlines to note:

- 31 March 2022 – 6-month SIBOR will be discontinued

- 30 June 2023 – SOR will be discontinued

- 31 December 2024 – 1-month and 3-month SIBOR will be discontinued

Since August 2020, The MAS started publishing the compounded rates for 1-month, 3-month, 6-month and a SORA index. This assures customers that the floating rates are derived from a transparent and reliable source.

2. SORA has been around since 2005

Contrary to what people may believe, SORA isn’t a new kid on the block. The Monetary Authority of Singapore (MAS) has been publishing daily SORA rates since July 2005.

The Association of Banks in Singapore describes The Singapore Overnight Rate Average (SORA) as the volume-weighted average rate of borrowing transactions in the unsecured overnight interbank SGD cash market in Singapore between 8 am and 6.15 pm.

After the data has been validated, it is published by 9 am on the next business day. MAS reviews the list of reporting banks regularly to ensure SORA stays robust and representative of the benchmark rate.

3. SORA is predictable and stable

When comparing how SORA calculates interest rates compared to SIBOR, SORA takes past transactions, whereas SIBOR looks at future transactions.

This means that with SORA, you can know what to expect next month. SIBOR is more volatile as banks can decide to increase or decrease future interest rates without warning. You won’t be surprised by unexpected rate hikes.

How it differs from SOR. For borrowers, the averaging effect from compounded SORA will provide significantly more stable rates than single-day SOR readings. SOR rates are regularly exposed to temperamental market factors, such as quarter or year-end volatility.

Unlike SOR, SORA transacts based on SGD, removing the need to account for the constantly fluctuating foreign exchange rates.

How it differs from SIBOR. SORA operates based on calculating the rate of all interbank lending transactions versus SIBOR, where it takes 20 banks. This makes the process a whole lot more transparent and less complicated.

4. SORA-pegged rates are currently pretty attractive

Currently, SORA rates are pretty attractive due to the current low interest-rate environment. Although it has been slowly increasing, the 3-Month Compounded SORA is 0.2086% p.a. as of 4 February 2022.

The all-in nett rate of the loan works out to be 1.2086% p.a., assuming the bank charges a spread of 1%.

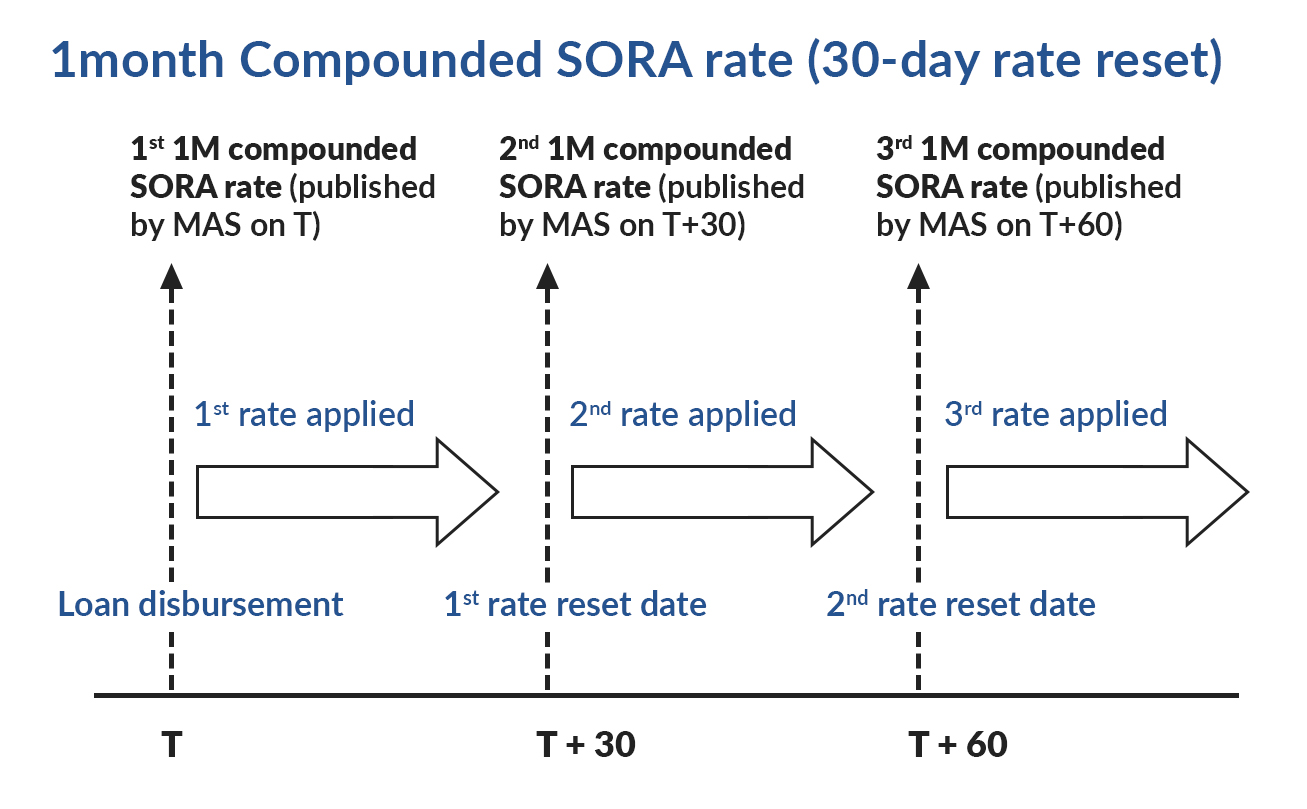

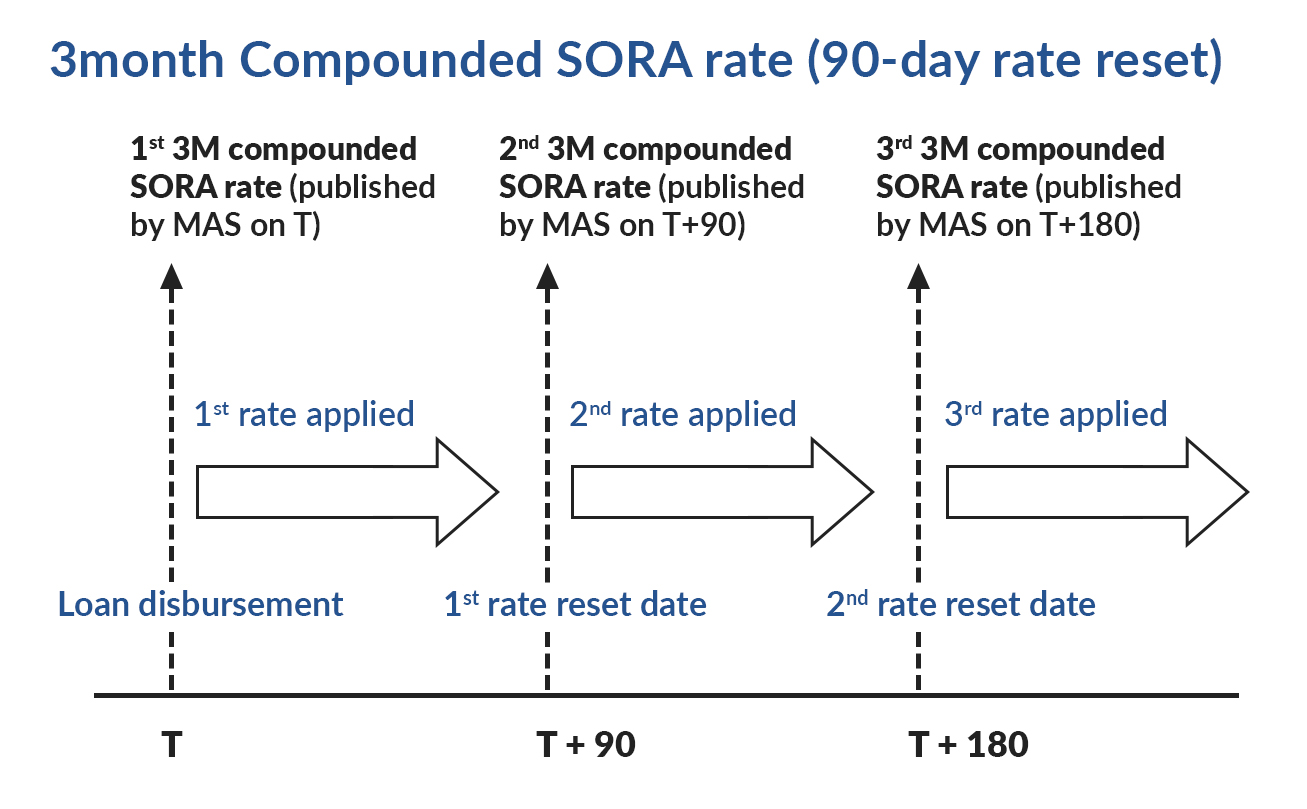

5. Calculating compounded SORA

Most SORA loans in the market are based on the 1-month or 3-month compounded rate. Advance compounding provides notice of the applicable interest rate and the monthly instalment payable for the upcoming period until the next rate reset date.

Knowing the instalment amounts in advance lets you plan your finances better.

Here is how the 1-month and 3-month compounded SORA rates are calculated for a loan package with a 30-day rate reset, and a 90-day rate reset respectively.

Depending on your bank’s internal processes, Day “T” refers to the date of loan disbursement or acceptance of the letter of offer, etc. Banks may also apply a 1-month Compounded SORA rate from a prior 30-day period which is not immediately preceding day “T” and each rate reset date, according to each bank’s internal processes.

What you should do if you currently have a SOR loan

If you currently have a SOR loan, your bank should be contacting you over the next couple of months and provide options to convert your SOR loan no later than 31 October 2022. This is so you won’t be disrupted by the discontinuation of SOR after 30 June 2023.

There should be no administrative or conversion fees payable, as well as a lock-in period when you decide to take up the SORA Conversion Package.

The SORA Conversion Package has three components, including:

3-month compounded SORA. The 3M compounded SORA is the most commonly offered default for SORA loan packages. It evens out rate volatility by taking the compounded average of daily SORA over the previous three months.

However, due to it being a floating reference rate, your monthly interest payments will fluctuate slightly. If you’re more risk-averse and prefer something more predictable, you have the option of switching to a fixed-rate loan package instead.

Should there be an unexpected hike in interest rates, you can keep calm and not panic as you’ll be paying the same amount regardless of any fluctuations. Do note that switching to a fixed-rate loan means your LTV and TDSR will be recalculated based on the latest cooling measures.

Your current SOR margin. Banks will carry your existing SOR margin in the SORA conversion package to ensure your new loan is comparable to your previous loan.

Adjustment spread. Published monthly on the first business day from 1 September 2021 until 1 September 2022, this spread reflects the average difference between SOR and compounded SORA-in-advance over three months before being published.

Every bank will have a different Adjustment Spread, so you are encouraged to contact your respective banks for more information about switching out your SOR loan early.

It’s best to stay informed and plan ahead prior to switching out your loans or opting for a fresh loan. Consult a specialist, such as a mortgage broker or your bank, so you’ll have an expert to walk you through the different options and loans available.

99.co also has a handy mortgage assistant so you can make the best-informed decision on your mortgage loans.

Any thoughts about switching over to a SORA-pegged loan? Let us know in the comments section below or on our Facebook post.

If you found this article helpful, check out 9 things about SORA for home loan interest rates and MAS begins transition from SOR to SORA.

Looking for a property? Find the home of your dreams today on Singapore’s fastest-growing property portal 99.co! If you would like to estimate the potential value of your property, check out 99.co’s Property Value Tool for free. Also, don’t forget to join our Facebook community page! Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

The post SORA-pegged home loan: 5 key things to know if you’re switching from SOR or SIBOR appeared first on 99.co.