Determining your loan eligibility for a home loan is arguably the most important part of planning for your property investment. Whether you’re a seasoned property investor or not, it’s important to do your research before buying property. You don’t want to make poor financial decisions or being misled into deals to avoid Additional Buyer’s Stamp Duty (ABSD).

According to our Singapore Consumer Sentiment Study H1 2024, the desire to buy an investment property in Singapore remains strong. 52% of homeowners aged 22 to 29 wanted to purchase an additional property while keeping their current property; similarly, 44% of homeowners aged 30 to 39 agreed.

To help aspiring property owners like yourself, we’ll walk you through the steps to take to properly plan for a property investment.

1. Perform a Financial Health Check

The first thing you’ll want to do is assess your financial situation to determine mortgage affordability.

Factors which will affect your loan eligibility for a home loan and determine mortgage affordability are your current income, monthly expenses, savings, credit score, and outstanding loans and debts.

Seeing how many aspiring property investors are under 40, we’ll assume a gross monthly income of $10,000. We used this number because, according to the Labour Force in Singapore 2023 report, the median monthly household income among resident employed households, excluding employer CPF contributions is $9,646.

The ideal situation you want to be in is you have a great credit score to up your chances of getting pre-approved on a loan. You’ll also have a healthy amount of cash and CPF savings. Maybe you have a car loan or a mortgage you’re still servicing, but that’s okay. But the most important thing is to be honest about your current financial situation.

Once you’ve got that down, the next thing to do is figure out your loan eligibility for a home loan. You need to answer the question “for a home loan, how much I can borrow?”

2. Know How Much You Can Potentially Loan

Consider Your TDSR and MSR

| 55% TDSR threshold | $5,500 in monthly instalments |

| 30% MSR limit | $3,000 in monthly installments |

The Total Debt Servicing Ratio (TDSR) states your total debt repayments cannot be more than 55% of your gross monthly income. If you currently own an HDB flat and are servicing a home loan for it, you’ll need to also consider the Mortgage Servicing Ratio (MSR). The MSR states the monthly repayment instalments for all your property loans can only be a maximum of 30% of your gross monthly income.

Already, you can see how the TDSR and MSR affects how much you can borrow for a home loan and loan eligibility for a home loan.

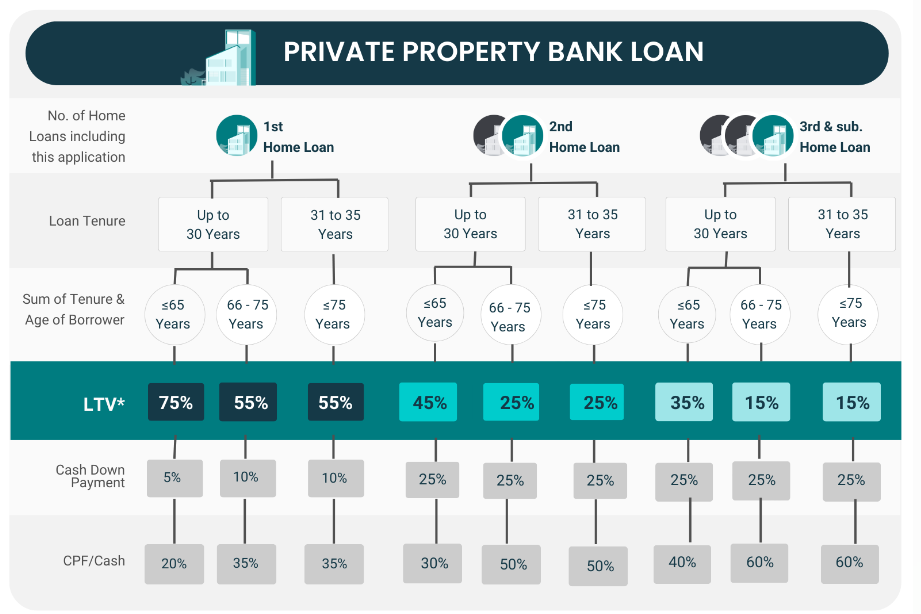

Check Your LTV Limit

The next thing to consider is the Loan-to-value (LTV) limit. Your LTV decreases with the number of housing loans you take on simultaneously.

According to Monetary Authority of Singapore (MAS) rules, the lower LTV limit is applied if the loan tenure is more than 30 years (or more than 25 years for HDB flats), or if the loan period extends beyond the borrower’s age of 65 years. That means if you want a mortgage with a longer loan tenure, your LTV and loan eligibility for a home loan will be affected if you’re older.

First-time investors are likely those who want to own an HDB flat and condo at the same time. If this is your situation, be extra mindful of the two ratios. As how much you can borrow for a home loan is lesser, owning a second property would require you to come up with a fair bit of cash upfront. The maximum LTV limit you’ll likely qualify for is 45%, which means you’ll have to fork out a 25% minimum cash down payment.

3. Get Pre-approved for a Home Loan

At this point, you may be wondering: where can I check my loan eligibility for a home loan? Do I have to manually calculate the loan amount I qualify for? The good news is you can use online tools like our PropertyGuru Finance Affordability Calculator to receive an estimate and check your loan eligibility for home loan.

Knowing how much you can borrow for a home loan, will help you budget better and know what your price range is. For example, if you are a couple in your forties purchasing a private property, your maximum loan tenure will be 25 years for a loan with a 75% LTV limit.

Assuming your combined household income is $10,000, you’ll be able to loan up to $964,000. Anything else, you’ll have to fork out cash.

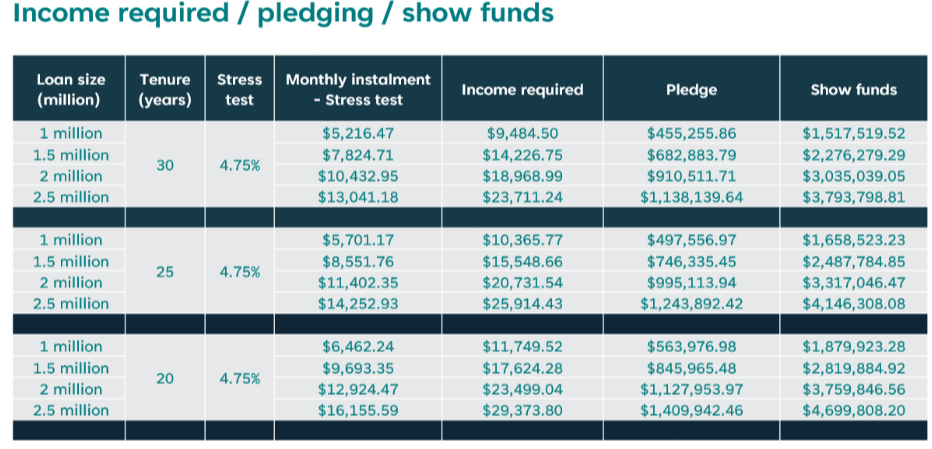

Here’s a general income to loan ratio guide here. Note that the MAS has a medium-term interest rate floor at 4.0% but banks have a higher stress-test interest rate. That’s why we used an interest rate of 4.75% for our calculations:

From there, you can go on to get pre-qualified for a home loan and receive an In-principle Approval (IPA) for your desired mortgage. Obtaining an IPA can show sellers you are a serious buyer and increase your chance of securing your desired property.

If you run into any questions on your loan eligibility for a home loan or need any home financing advice, you can always reach out to our team of dedicated Mortgage Experts (it’s free!).

4. Browse Properties within Your Budget

At this point, you’ve got your loan eligibility for a home loan down and all the numbers are out of the way. It’s time for the fun part: browsing property listings!

Here’s a tip: use our Home Value Tracker to evaluate property prices and trends in target areas. This way, you know if you’re getting a good deal and better negotiate with sellers.

Using the above example, a couple who obtain a $964,000 loan can look for properties below $1,280,000.

But wait! There are additional fees you have to pay such as stamp duties and legal fees. Assuming you are buying $1,280,000 have at least $256,000 in your CPF OA, you’ll still have to fork out $391,500 in cash. Here’s a breakdown:

| 5% of the property purchase price in cash (minimum cash down payment required) | $64,000 |

| 20% of the property purchase in CPF/cash (rest of the down payment) | $256,000 |

| Buyer’s Stamp Duty (BSD) | $35,800 |

| Additional Buyer’s Stamp Duty (ABSD), assuming you are both Singaporean and this is your second property owned | $291,800 |

| Legal fees | $3,000 |

| Estimated valuation fees | $500 |

You can use our Stamp Duty Calculator to figure out how much BSD and ABSD you’ll have to pay.

What If My Dream Home Is More than What I Can Loan?

If your dream home is more than what your loan can get, you will have to make up for the difference in cold, hard cash. When you determine mortgage affordability, it’s less likely you’ll run into this problem.

Some ways to improve your loan eligibility for a home loan is to pay down debts and improve your credit score (if required). By improving your financial health, your loan eligibility for home loan goes up and buying an investment property becomes less of a financial stretch.

Buying a property investment can be a great way to build wealth but you need to determine mortgage affordability and do careful planning before taking the plunge. Making an informed decision starts by asking yourself: can I truly afford a second property investment in Singapore? And if you need home financing advice from an expert, do not hesitate to reach out for help.

Chat with us on WhatsApp

Fill up an online form