As US interest rates continue to rise, the Monetary Authority of Singapore (MAS), Ministry of National Development (MND) and Housing and Development Board (HDB) have taken a pre-emptive step to introduce new cooling measures (albeit ‘temporary’ and subject to continuous review and updates).

The move is aimed at promoting more prudent borrowing and avoiding future difficulties for homeowners to service their home loans.

As mortgage interest rates pegged to the 3-month Compounded Singapore Overnight Rate Average (SORA) continue to rise, the government expects this rise to continue into 2023 along with rising US interest rates, before settling at a higher level (compared to previous lows between 2013-2021).

Here then are the measures:

1. Higher medium-term interest rate floor for bank and HDB housing loan eligibility

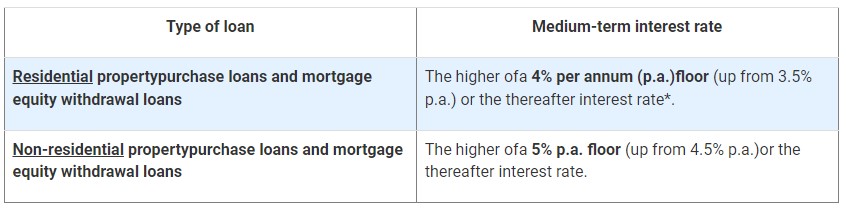

a. For property loans from private financial institutions (eg. banks), MAS will raise the medium-term interest rate floor to compute the Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) by 0.5% point.

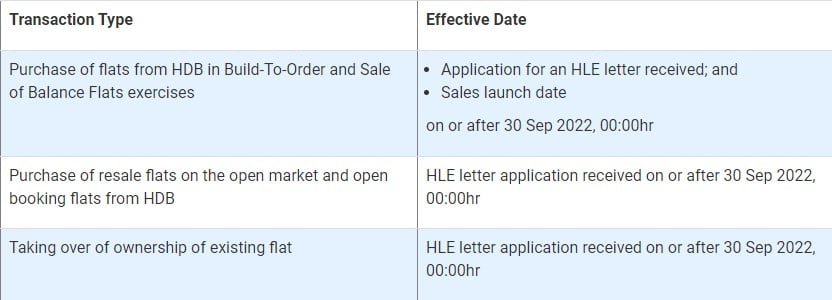

- This applies to loans for the purchase of properties where the Option to Purchase (OTP) is granted on or after 30 September 2022. If there is no OTP, then for Sale and Purchase Agreements dated on or after 30 September 2022.

- While there is an interest rate floor for calculating TDSR and MSR, private financial institutions will ultimately still determine the actual interest rates charged for mortgages.

From 30 September 2022, banks will calculate applicants’ TDSR and MSR from a new medium-term interest rate – such as the higher 4% per annum floor or thereafter interest rate (for residential property purchase loans and mortgage equity withdrawal).

b. For housing loans granted by HDB, HDB will introduce an interest rate floor of 3% for computing eligible loan amounts.

- The interest rate floor applies to fresh applications for an HDB Loan Eligibility (HLE) letter received on or after 30 September 2022, 00:00 hours.

- This will not impact existing HLE applications received by HDB before this time.

- This does not affect the actual HDB concessionary interest rate, which remains unchanged at 2.6% per annum.

2. Lower Loan-to-Value limit for HDB housing loans (85% to 80%)

Loan-to-Value limit for HDB housing loans will be lowered from the previous 85% to 80%. This lower LTV limit applies to new flat applications for sales exercises launched (including the upcoming HDB BTO November 2022 launch) and completed resale applications received by HDB on or after 30 September 2022.

3. 15-month Wait for Private Property Owners (below 55 years old) buying non-subsidised HDB resale flat

To moderate demand in the HDB resale market, there is now a wait-out period of 15 months for private residential property owners (PPOs) and ex-PPOs to buy a non-subsidised HDB resale flat.

What this means is that private homeowners who are buying a non-subsidised HDB resale flat from the open market will not only have to dispose of their private properties, but they also have to wait 15 months after the disposal of their private properties before they are eligible to buy the non-subsidised HDB resale flat.

While this is a temporary measure to moderate demand for resale flats (for example, million-dollar resale HDB flats), the agencies will continue to review overall demand and market changes when necessary. Note that the wait-out period for PPOs who are first-timers and wish to apply for CPF Housing Grant and Enhanced CPF Housing Grant for their flat purchase remains unchanged at 30 months.

There is some good news, however.

For seniors aged 55 and above who move from their private property to a 4-room or smaller resale flat, the wait-out period will not apply to them. Senior PPOs/ex-PPOs can buy a 2-room Flexi flat on short lease (if aged 55 and above) and Community Care Apartment (if aged 65 and above) from HDB. They can also approach HDB for assistance if they face extenuating circumstances (eg. financial difficulties).

This new measure takes effect from 30 September 2022. This is a temporary measure which will be reviewed in the future depending on overall market conditions and demand.

–

According to the agencies, these measures are not expected to affect first-timer and lower-income flat buyers significantly, as they may receive housing grants of up to S$80,000 when buying a subsidised flat directly from HDB, or up to S$160,000 when buying a resale flat.

They can also tap on their CPF savings to pay for their flat purchase, which would reduce the loan amount they need to take.

–

How the above changes will impact Private Property Home Loan Borrowers

The changes above will affect the maximum amount a borrower can loan. The simulation below shows that borrowers’ maximum loan amount will reduce by 5.9% if comparing the medium-term rates before and after 30 September 2022 for the purchase of a private property.

So from an estimated maximum loan of S$1,224,823 before 30 September (at a medium-term rate of 3.5%), the new maximum is now estimated to be at S$1,152,037 (at 4.0%).

Home buyer buying a private property before and after 30 September 2022

| Estimated maximum loan | Estimated maximum purchase price | Estimated monthly installment | |

| Medium Term Rate 3.5% | S$1,224,823 | S$1,633,097 | S$4,935 |

| Medium Term Rate 4.0% | S$1,152,037 | S$1,536,049 | S$4,639 |

| Absolute Difference | S$72,786 | -S$97,047 | -S$296 |

| Percentage Difference | -5.90% | -5.90% | -6.00% |

- Assuming: S$10,000 gross monthly income and loan tenure of 30 years for maximum loan amount

- Assuming 3-month SORA interest rate loan at 2.65% and loan tenure 30 years

** Source: Huttons Research

For the same property, buyers are forced to cough up more in upfront cash to make up the difference. This will have some impact on demand as they hold back on their purchases.

“Developers may defer some launches to next year,” said Mr Lee Sze Teck, Senior Director (Research), from Huttons Asia. “Transaction volume may be slower in the next three months. We will probably see new sales transaction volume of around 8,000 units, lower than our initial forecast of up to 9,000 units in 2022.”

However, Lee does not think prices are likely to be affected. “For existing launches in the market, most of them have sold 80% or more of their units, and it will be business as usual.”

How the above changes will impact HDB Home Loan Borrowers

With the changes to the HDB floor rate and lower LTV ratio for HDB concessionary loans (85% to 80%), the loan amount HDB buyers can borrow is smaller and should be able to be covered through grants. The example below reflects the difference if a buyer purchases an HDB flat and applies for an HDB home loan (from a bank) before and after 30 September 2022.

Home buyer buying an HDB flat before and after 30 September 2022

| Estimated maximum loan | Estimated maximum purchase price | Estimated monthly instalment | |

| Medium Term Rate 3.5% | S$359,552 | S$479,402 | S$1,640 |

| Medium Term Rate 4.0% | S$341,014 | S$454,686 | S$1,556 |

| Absolute Difference | -S$18,537 | -S$24,716 | -S$84 |

| Percentage Difference | -5.20% | -5.20% | -5.10% |

– Assuming: S$6,000 gross monthly income and loan tenure of 25 years for maximum loan amount

– Assuming an interest rate of 2.65% and loan tenure 25 years

** Source: Huttons Research

“The spate of million-dollar flats transactions in recent months were partly driven by private property owners. Many of them paid for the resale HDB flats in cash without the need for a loan. This has an overall uplifting effect on the HDB resale market,” said Lee.

He expects HDB resale prices to likely stabilise further in Q4 2022 and forecasts no more than a 10% increase in price and volume in 2022.

–

3

2

2

2

3

4

2

2

3

3

2

2

3

2

2

2

3

2

2

3

3

2

0

1

2

2

3

2

3

3

3

3

3

3

3

3

2

2

3

3

–

FAQs on New Property Cooling Measures 2022

The three key measures are a higher medium-term interest rate floor for bank and HDB housing loan calculations, lower loan-to-value limit for HDB housing loans and a 15-month wait for private property owners intending to buy a non-subsidised HDB resale flat.

For financial institutions like banks, the floors are 4% per annum or thereafter for residential properties and 5% per annum for non-residential properties. For HDB housing loans issued by HDB, it will be 3%.

The rule applies to private residential property owners (PPOs) and ex-PPOs (aged 54 and below) who are buying a non-subsidised HDB resale flat (any size). For seniors aged 55 and above, the rule applies if they intend to buy a 5-room or executive resale flat. They will have to wait 15 months after selling their private properties before they’re able to buy a non-subsidised HDB resale flat.

What are your thoughts on these new financial prudence cooling measures? Let us know in the comments section below.

If you found this article helpful, 99.co recommends Cooling measures announced – ABSD, TDSR and LTV – effective from midnight 16 December 2021 and How will the new cooling measures affect property activity?

Related Articles:

The post New property cooling measures (September 2022): Borrowing restrictions and lower LTV limit to affect home loan applicants and private-to-HDB resale flat buyers appeared first on .