It’s been over a month since the government rolled out the cooling measures on 16 December. The news might not be hot off the press anymore – property analysts and agents have chimed in and given their two cents worth – but what do Singaporeans think about it?

ABSD increase

One thing that everyone unanimously agreed on was the increase in Additional Buyer’s Stamp Duty (ASBD).

| Types of Buyers | Rates from 6 July 2018 to 15 December 2021 | Rates on or after 16 December 2021 | |

| Singapore Citizens | First residential property | 0% | 0% |

| Second residential property | 12% | 17% (+5%) | |

| Third and subsequent residential property | 15% | 25% (+10%) | |

| Permanent Residents | First residential property | 5% | 5% (unchanged) |

| Second residential property | 15% | 25% (+10%) | |

| Third and subsequent residential property | 20% | 30% (+10%) | |

| Foreigners | Any residential property | 20% | 30% (+10%) |

| Entities | Any residential property | 25% | 35% (Plus additional 5% for housing developers (non-remittable)) (+15%) |

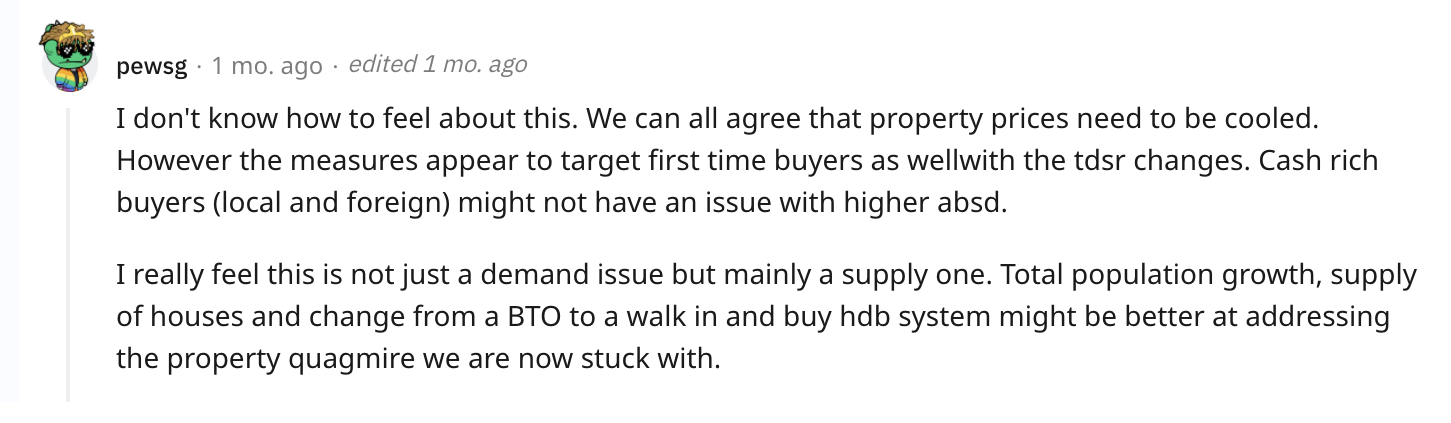

The rise in ABSD mainly affects private property speculators eyeing their next property and foreigners purchasing their first property. Some felt that cash-rich buyers who have money to splash would probably not have a huge issue with the six-figure ABSD hike on a million-dollar property as the potential gain would far outweigh the ABSD payable.

Others saw the new ABSD targeting foreign buyers who see Singapore as a safe haven to park their money in, given some countries’ pandemic-induced economic instability.

TDSR tightening

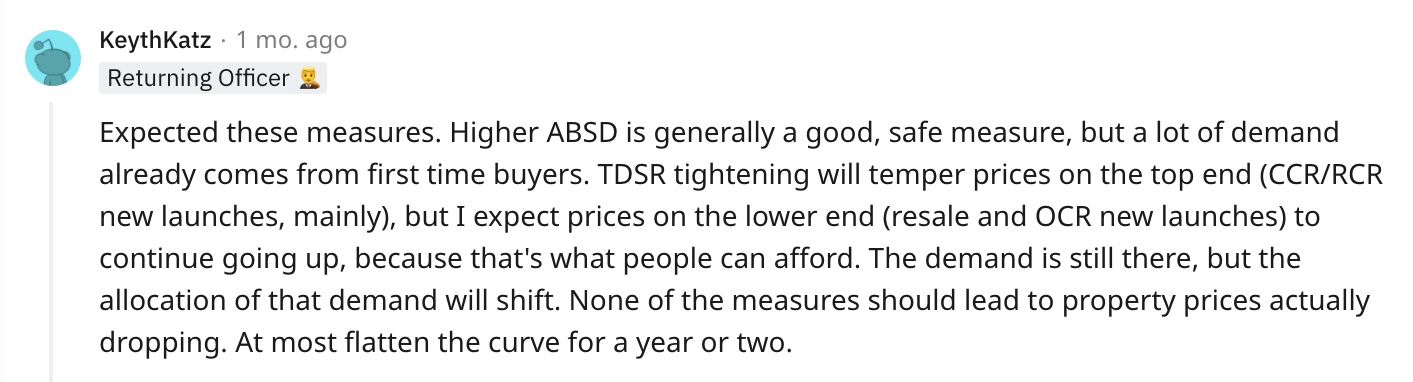

The Total Debt Servicing Ratio (TDSR) threshold was tightened by 5 points to 55%, down from the previous 60%. Monthly loan repayments of borrowers cannot exceed 55% of their monthly income. Such obligations include student loans, car loans and credit card payments.

Some commenters on Reddit Singapore and HardwareZone forum speculated that tightening the TDSR won’t temper the demand, but instead shift its allocation. It may force down high prices for Core Central Region (CCR) and Rest of Central Region (RCR) properties and new launches, but prices for Outside Central Region (OCR) houses will continue to increase due to its affordability.

| Year | CCR S$/psf | RCR S$/psf | OCR S$/psf |

| 2019 | 2,330 | 1,716 | 1,274 |

| 2020 | 2,203 | 1,676 | 1,296 |

| 2021 | 2,344 | 1,804 | 1,320 |

The numbers back it up, too. As indicated in the above table, the average cost per square foot of condos in the OCR has consistently been more than half that of condos in the CCR area, making it a more affordable choice.

Some deduced that the reduced limit is aimed to taper off demand from buyers who are stretching their budget to the limit of their TDSR. We agree that it is crucial to be financially prudent, especially when there are strong indicators of increased interest rates in the near future.

With the US Federal Reserve tapering bond purchases and moving closer to a rate hike, Singapore’s domestic interest rates is bound to increase as global market movements from major economies largely influence our little red dot.

LTV cap

The Loan to value (LTV) limit for both new and resale HDB loans have tightened from 90% to 85%.

This may have been a calibrated move from the government to taper the rapidly rising and record-smashing HDB resale prices. 2021 saw HDB resale prices skyrocketing by 12.7%, ending the year on an all-time high. 259 resale flats were transacted for more than S$1 million, the highest number on record so far.

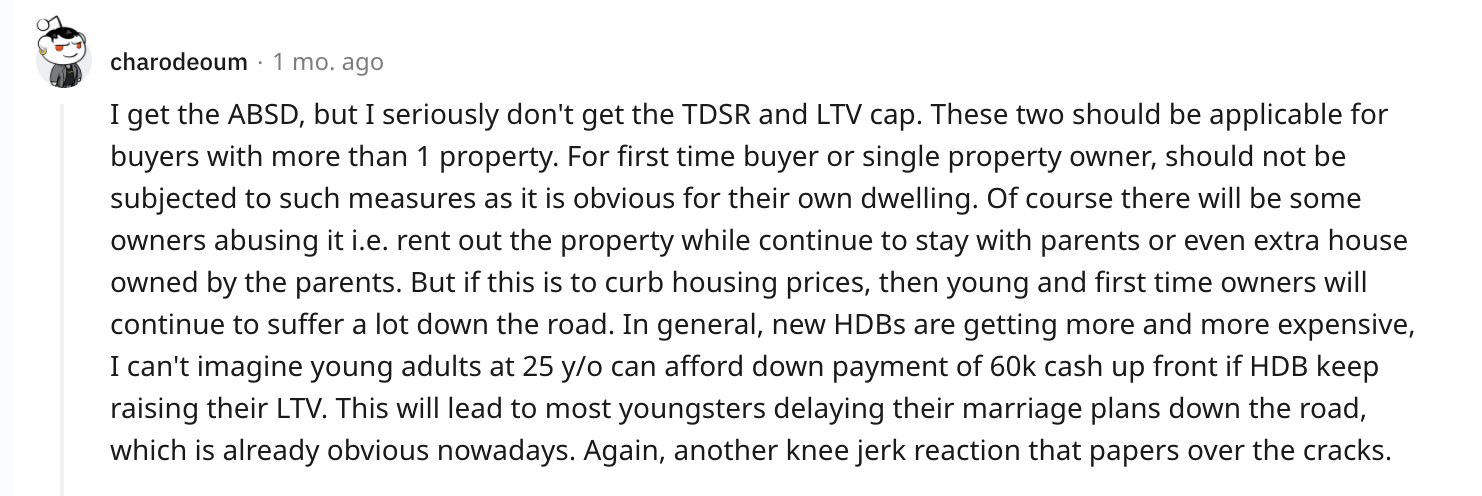

There was common sentiment amongst users that the LTV should only affect buyers who currently own more than one property. First-timers should be excluded as they are most likely genuine homebuyers looking for their first property. A tighter LTV raises the barrier even higher for the average cash-strapped first-time homeowner.

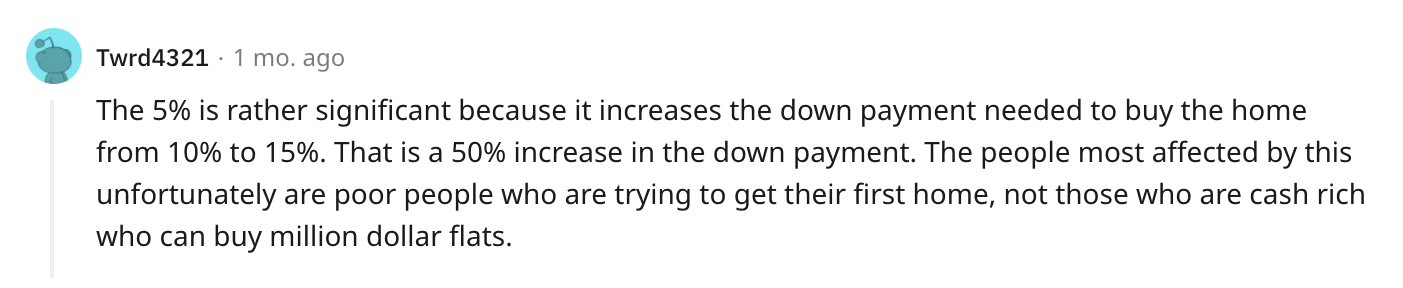

Tightening the LTV by 5% is significant, increasing the initial downpayment from 10% to 15%. Most first-time homebuyers are young millennials leaving the nest or couples starting new families looking for their first home. These groups usually start their lives with a lower salary and may not be able to afford the increased upfront downpayment with the LTV hike.

Take a S$500,000 BTO flat as an example. With the tightened LTV, the downpayment would now be S$74,000 instead of S$50,000.

On the flip side, other forum users pointed out that this meant filtering out reckless buyers who don’t think twice about taking on a bigger loan and those who pick HDB flats solely based on investment potential.

Increasing the LTV forces homebuyers to assess what they can comfortably afford instead of what they want. They reasoned that if the 5% increase was so significant that the house purchase had to be delayed, buyers were probably over-leveraging or being picky with neighbourhoods, such as going for a 5-room instead of a 4-room flat.

Homeowners should exercise due financial diligence and choose what suits their current budget as they can always upgrade in future, like this Reddit user pointed out.

BTO delays

Pent up demand from BTO delays has also seen more pivoting to the resale market. With work-from-home fast becoming the norm, more people are looking to move out of their family homes in search of more privacy and space.

HDB is addressing this issue by increasing public and private housing supply to promote a more stable property market. An increase in HDB supply alleviates the problem of skyrocketing HDB prices, giving young Singaporeans more chances to acquire affordable housing.

Minister for National Development Desmond Lee stated that the supply of BTO flats will be ramping up to launch 23,000 flats per year in 2022 and 2023, a 35% increase from the 17,000 flats launched in 2021. Hopefully this reduces oversubscription rates, especially in popular housing estates such as Clementi, Bishan and Ang Mo Kio.

Decentralisation

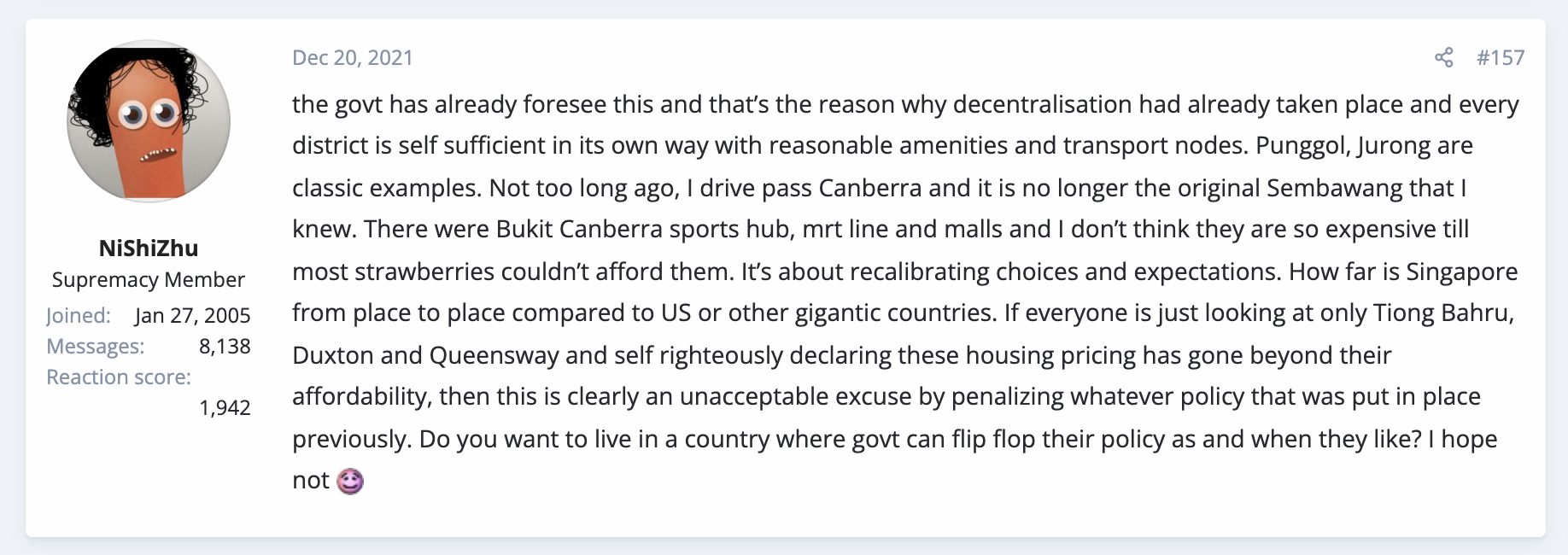

One interesting issue that a user brought up is decentralisation in Singapore.

Over the years, the government has focused its efforts on building up each neighbourhood to ensure that every district is self-sufficient, with reasonable amenities and transport nodes.

This is a stark contrast from years ago, when you had to travel out to access amenities, retail and entertainment options. It is why Singapore has its URA Master Plan reviewed every five years to ensure Singapore’s sustainability going into the future.

Decades ago, Singapore reviewed its 1991 Concept Plan to ease traffic congestion in and out of The Central Business District during peak hours. URA mapped out a long-term decentralisation strategy to distribute commercial activities nationwide and reduce the need to travel.

As such, homebuyers should recalibrate their choices and expectations and consider living in more affordable OCR neighbourhoods instead of focusing their sights on expensive districts such as those in the CCR and RCR, such as Queenstown, Tanjong Pagar and Tiong Bahru.

Due to its land scarcity, Singapore’s decentralisation efforts might benefit from building more mixed-use developments in more districts to cater to the needs of the residents living in those neighbourhoods and make them more attractive to potential homebuyers, thus flattening the rise of property prices in CCR districts.

An example of a mixed-use development in the OCR is Le Quest, a 99-year condo located in Bukit Batok. It is located on top of a shopping mall, and with the Tengah Park MRT set to open in 2027, it has great potential to accrue in value.

General consensus amongst the community

Given that any significant price changes are highly unlikely to be immediate, those who urgently need to acquire housing will be the most affected. The majority of people on the ground agreed that the cooling measures aimed to dampen demand from foreigners and speculators.

At the same time, the property price curve will stay flattened for a year or two due to housing demand being inelastic as people will always need a roof over their heads.

Do you have any opinion about the cooling measures? Let us know in the comments section below or on our Facebook post.

If you found this article helpful, check out 5 things every homebuyer must do if new cooling measures are suddenly announced and How to decode the URA Masterplan.

Looking for a property? Find the home of your dreams today on Singapore’s fastest-growing property portal 99.co! If you would like to estimate the potential value of your property, check out 99.co’s Property Value Tool for free. Also, don’t forget to join our Facebook community page! Meanwhile, if you have an interesting property-related story to share with us, drop us a message here — and we’ll review it and get back to you.

The post You’ve heard analysts and agents, but what are some community feedback on the cooling measures? appeared first on 99.co.