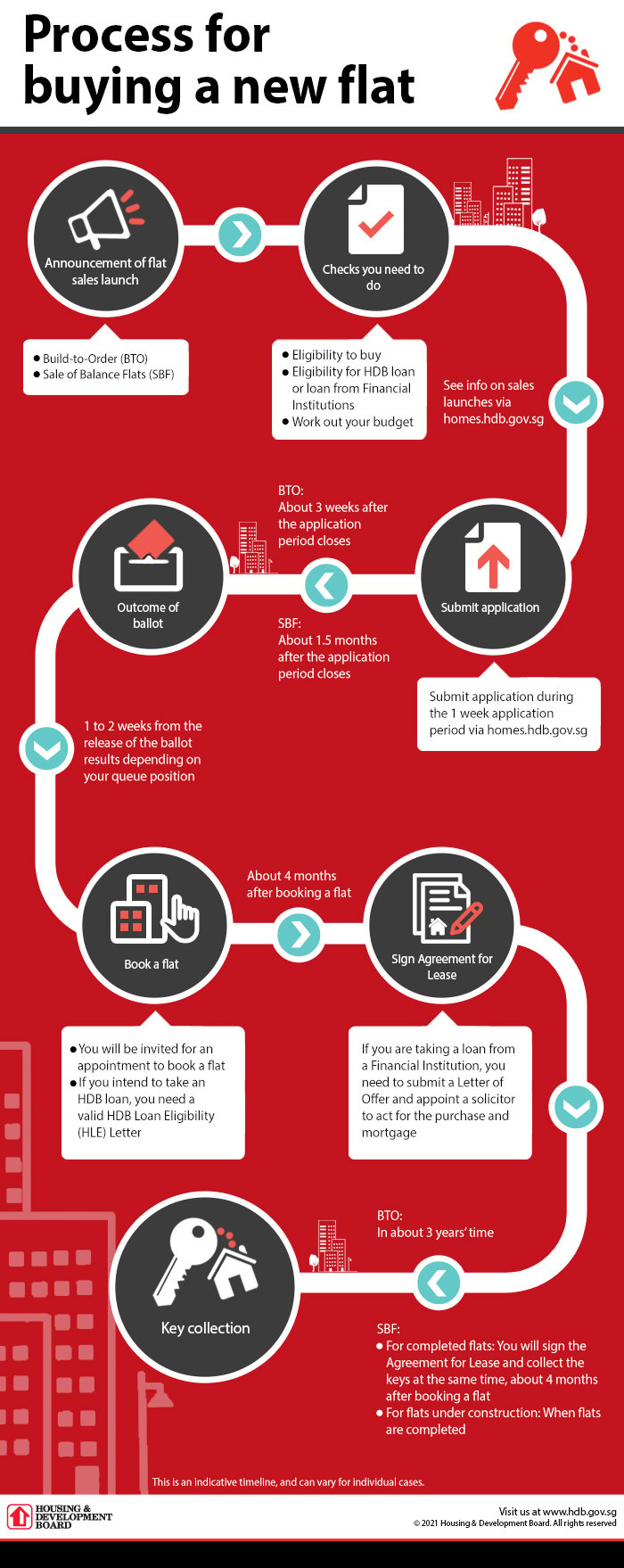

Buying a BTO flat is almost a rite of passage for new couples in Singapore. But with the excitement of owning a home, comes the scary part: the BTO payment timeline to pay for the flat.

That’s why our top advice for prospective homebuyers is to make sure that their finances are sorted before applying for a BTO. This ensures that they’re able to afford the payments when they’re due.

For that reason, we’ve come up with this little cheat sheet summarising the BTO payment timeline help you figure out what you’re in when you sign the dotted line.

HDB BTO payment timeline

| Stage of purchase | Fees payable | Amount payable | Payment mode |

| BTO application | Application fee | S$10 | Credit card or mobile payment app (eg. DBS PayLah!, UOB Mighty, OCBC Pay Anyone, etc.) |

| Flat booking | Option fee (forms part of the downpayment) | 2-room Flexi: S$500 | NETS |

| 3-room: S$1,000 | |||

| 4-room and bigger: S$2,000 | |||

| Signing of Agreement for Lease | Stamp duty | First S$180,000: 1% | Cashier’s Order, CPF |

| Next S$180,000: 2% | |||

| Next S$640,000: 3% | |||

| Remaining amount: 4% | |||

| Conveyancing fee | First S$30,000: S$0.90 per S$1,000 | ||

| Next S$30,000: S$0.72 per S$1,000 | |||

| Remaining amount: S$0.60 per S$1,000 | |||

| Downpayment | If taking HDB loan: 10% of purchase price | ||

| If taking bank loan with LTV of 75%: 5% cash, 15% CPF and/or cash | |||

| If taking bank loan with LTV of 55%: 10% cash, 10% CPF and/or cash | |||

| Key collection | Registration fee | Lease In-Escrow: S$38.30 | Cashier’s Order, CPF |

| Mortgage In-Escrow: S$38.30 | |||

| Survey fee | 1-room: S$150 | ||

| 2-room: S$150 | |||

| 3-room: S$212.50 | |||

| 4-room: S$275 | |||

| 5-room: S$325 | |||

| Executive: S$375 | |||

| Stamp duty for Deed of Assignment | 0.4% of the loan amount, up to S$500 | ||

| Home Protection Scheme | If you’re using CPF to pay for loan instalments, depends on factors like outstanding loan | ||

| Fire insurance | If you’re taking HDB loan, from S$1.62 to S$8.10 for five years | ||

| Balance of the purchase price | If taking bank loan with 75% LTV: 5% of purchase price with CPF and/or cash | ||

| If taking bank loan with 55% LTV: 25% of purchase price with CPF and/or cash |

Here’s an illustration for taking an HDB loan

Let’s take the example of newlywed couple Mark and Sophie, who are both Singapore Citizens in their 20s.

They are first-timer applicants with a combined income of S$5,000/month looking to purchase a 3-room BTO Flat, with a purchase price of S$300,000.

They also qualify for the Staggered Downpayment Scheme (SDS), and will be financing their purchase with an HDB loan which will cover up to 90% of the purchase price, for a term of 25 years. They also intend to service their loan instalments using their CPF.

| Fees payable | Amount payable |

| Application fee | S$10 |

| Option fee (forms part of the downpayment) | S$1,000 |

| Stamp duty | S$4,200 |

| Conveyancing fee | S$206.08 (including GST) |

| Downpayment less option fee | 5% of purchase price minus option fee: S$14,000 (cash or CPF) |

| Registration fee | Lease In-Escrow: S$38.30 |

| Mortgage In-Escrow: S$38.30 | |

| Survey fee | S$212.50 |

| Stamp duty for Deed of Assignment | S$500 |

| Home Protection Scheme | S$132.30 annually |

| Fire insurance | S$4.87 for five years |

| Balance of the purchase price | Downpayment: 5% of purchase price: S$15,000 (cash or CPF) |

| S$270,000 (HDB loan) | |

| Total | S$305,342.35 |

If you’re taking a bank loan for your BTO

Now let’s see how the finances work out if they were to take out a bank loan with a 30-year tenure. Since it’s their first loan, they are entitled to a loan of up to 75% of the purchase price.

In this case, they decide to go with legal counsel that their bank recommends, at a cost of S$2,500.

| Fees payable | Amount payable |

| Application fee | S$10 |

| Option fee (forms part of the downpayment) | S$1,000 |

| Stamp duty | S$4,200 |

| Legal fees | S$2,500 |

| Downpayment less option fee | 10% of purchase price minus option fee: S$29,000 (5% cash + 5% cash or CPF) |

| Registration fee | Lease In-Escrow: S$38.30 |

| Mortgage In-Escrow: S$38.30 | |

| Survey fee | S$212.50 |

| Stamp duty for Deed of Assignment | S$500 |

| Home Protection Scheme | S$120.38 annually |

| Balance of the purchase price | Downpayment: 15% of purchase price: S$45,000 (cash or CPF) |

| S$225,000 (HDB loan) | |

| Total | S$307,619.48 |

What’s your experience with the HDB BTO payment process? Let us know in the comments section below or on our Facebook post.

If you found this article helpful, 99.co recommends 99.co’s guides: Buying a BTO – The Process & Procedures and My complete BTO experience: From balloting to renovation regrets.

[Additional reporting by Virginia Tanggono]

Frequently asked questions

What’s the downpayment for BTO?

If you’re taking an HDB loan, the BTO downpayment is 10% of the purchase price. If you’re taking a bank loan, the downpayment is 25%.

How long does a BTO project take to complete?

The wait time is usually three to four years. However, due to supply constraints, manpower shortages and delays, it can take around five years to complete.

How many times can you apply for BTO?

As long as you’ve not bought a new HDB, DBSS or EC, or received a CPF Housing Grant before, you can buy a BTO up to two times.

The post Everything you need to know about the HDB BTO payment timeline appeared first on 99.co.